State of Vietnam’s Textile and Clothing Industry

Vietnam has a substantial textile and clothing industry comprising around 4,000 enterprises, of which the majority were located in the country’s two principal population centers—Ho Chi Minh City and Hanoi. Around 70% of these enterprises were involved in the manufacture of clothing. A further 17% were involved in the fabric sector, 6% in the yarn sector, 4% in the dyeing sector and 3% in the accessories sector.

It is estimated that around 70% of Vietnam’s textile and clothing production is dependent on the cut and trims operations, using imported textiles and other inputs predominantly from China. This problem is not limited to a single category as the country needs to import man-made fibers, yarns, fabrics, and accessories as well as raw cotton.

The dyeing and finishing segments of the supply chain remain fairly underdeveloped. In the past, the Vietnamese government has issued tightly controlled permits for these operations. Also, there has been a deficiency of investment in these segments because of unclear regulations, and this has resulted in a bottleneck in the supply chain.

Similarly, high added-value design and “downstream” activities rely on the input of foreign companies are also underdeveloped. Consequently, in carrying out these activities, the industry relies heavily on the help or participation of foreign companies.

State of Vietnam’s Textile and Apparel Export

Vietnamese textile and clothing exports began to gain momentum in 2001 when trading relationships were established with Western countries (e.g., the US-Vietnam Textile Agreement). The industry’s exports received a further boost after Vietnam joined the World Trade Organization (WTO) at the start of 2007, and the quotas which had been restricting imports of Vietnamese goods in the US market were eliminated.

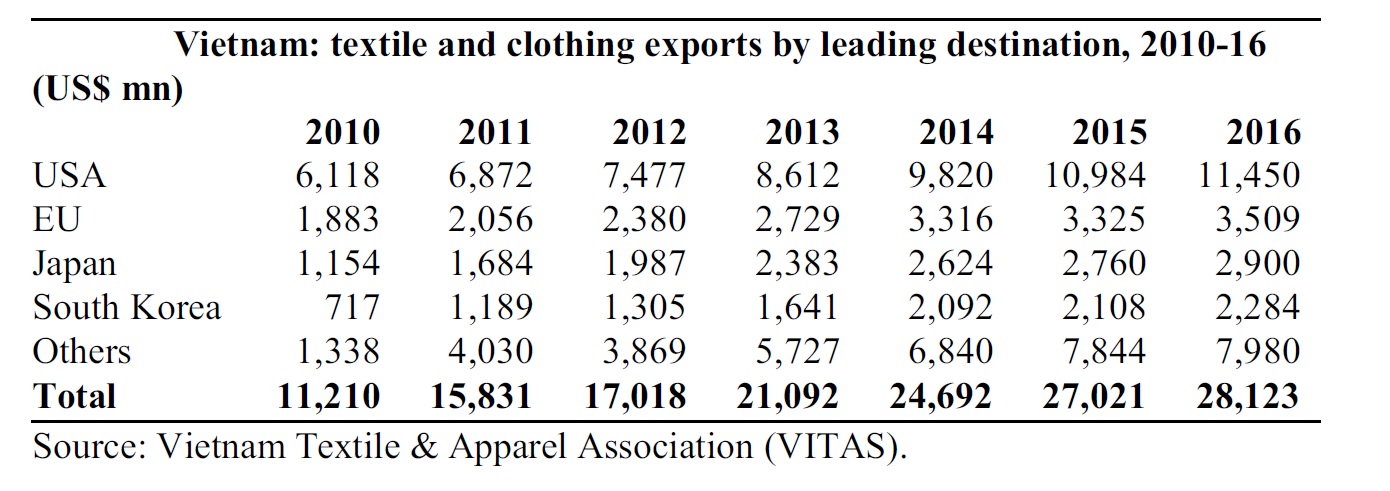

In 2016, Vietnam’s textile and clothing exports totaled $28 billion (84% were clothing), which represented 16.0% of Vietnam’s total merchandise exports. Globally, Vietnam was the world’s third largest apparel exporter in 2015, after China and Bangladesh (WTO, 2016).

The Vietnam Textile & Apparel Association (VITAS) expects Vietnam’s textile and clothing exports to enjoy an average 15% annual growth in the next four years and exceed $50 billion USD by 2020.

Vietnam’s textile and clothing exports went to around 180 countries. The United States is Vietnam’s top export market (around 40%), followed by the EU (around 12.5%), Japan (10.3%) and South Korea (8.1%).

Outlook of Sourcing from Vietnam by US Fashion Companies

According to the 2017 US Fashion Industry Benchmarking Study, Vietnam is the 2nd most used sourcing destination by respondents. Particularly, the most commonly adopted sourcing model is shifting from “China Plus Many” to “China Plus Vietnam Plus Many”:

- China typically accounts for 30-50 percent of respondents’ total sourcing value or volume.

- Vietnam typically accounts for 11-30 percent of companies’ total sourcing value or volume.

- For the “many” part, each additional country (such as US, NAFTA members and CAFTA members, EU countries and members of AGOA) typically accounts for less than 10 percent of respondents’ total sourcing value or volume.

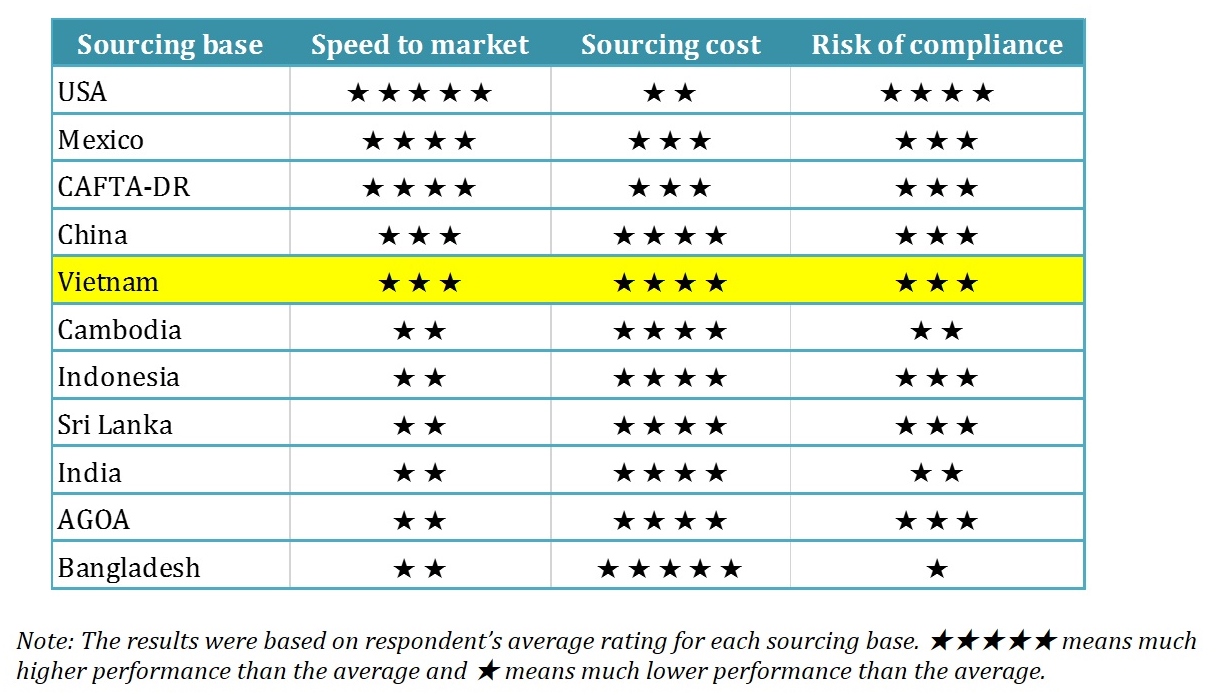

Respondents also see Vietnam overall a balanced sourcing destination, regarding “speed to market”, “sourcing cost” and “compliance risk”.

Additionally, U.S. fashion companies intend to source more from Vietnam through 2019, but imports may grow at a relatively slow pace, possibly due to the United States’ withdrawal from the Trans-Pacific Partnership (TPP) and the increasing labor costs in the country.

References:Textile Outlook International (2017); WTO (2017); UN Comtrade (2017)

A very insightful analysis. It would be useful to have an annual update.

Thank you @Sheng Lu

Thank you Mark! Surely will do.

The article says, “The dyeing and finishing segments of the supply chain remain fairly underdeveloped. In the past, the Vietnamese government has issued tightly controlled permits for these operations.” By not being able to complete this step of finishing a argument, I think Vietnam is loosing out. How can Vietnam go about changing this?

If I am correct, the fact that Vietnam’s textile and clothing production is dependent on cut and trim operations, receiving textiles from China, follows the flying geese model in the RPTN of Asia. This is because Vietnam is not as well developed in its economy therefore it does not make textiles yet like China does, which is more developed and has the position of a textile producer in the flying geese model and RPTN of Asia. This is why it stays within the region, with Asia sourcing from China rather than from places like the US, due to the flying geese model.

I agree that Vietnam still relies heavily on imported textiles because of its development stage. Here is a recent article from the Financial Times, FYI: https://www.businesstelegraph.co.uk/why-vietnam-must-move-up-the-clothing-value-chain/

Meanwhile, Vietnam is building its textile industry–thanks to the foreign investments. On the other hand, the geographic location makes it difficult for Vietnam to use US-made textiles–it would double the current lead time.